JULY TAX NEWS AND ADVICE

Published 18 July 2019

A STAFF SUMMER PARTY CAN BE A TAX-FREE BENEFIT

Your organisation may have an annual Christmas party for staff, but the tax rules also allow staff parties at other times of the year which are a tax-free benefit if certain conditions are satisfied.

The exemption applies to an annual party (for example, a Christmas party), or similar annual function (for example, a summer barbecue), provided for employees and is available to all employees or available to all employees at that location, where the employer has more than one location. If the employer provides two or more annual parties or functions, no tax charge arises in respect of the party, or parties, for which cost(s) per head do not exceed £150 in aggregate. For each function the cost per head should be calculated. The cost per head of subsequent functions should be added. If the total cost per head goes over £150 then whichever functions best utilise the £150 are exempt, the other is taxable.

MAKE SCHOOL HOLIDAYS EASIER WITH TAX-FREE CHILDCARE

Did you know there is a government scheme available that can help contribute towards childcare costs which may mean fewer of your employees will need time off at the same time this summer.

Tax-Free Childcare is a scheme available to working parents with children from 0-11 years and many parents are not taking advantage of the scheme. HMRC would thus welcome help from employers in changing that, so please tell your employees about Tax-Free Childcare and how it can reduce their childcare costs.

Eligible parents can get up to £2,000 per child, per year to spend on qualifying childcare (effectively a 25% top up). Note that Tax-Free Childcare isn’t just for everyday childcare costs, such as childminders and nurseries, parents can also use it to pay towards the cost of:

- after school clubs

- summer camps

- school holiday activities

USING A PAYE SETTLEMENT AGREEMENT TO PAY SOME OF YOUR EMPLOYEE'S TAX

PAYE settlement agreements (PSAs) are arrangements under which an employer can settle the income tax and National Insurance liabilities on benefits in kind and expenses payments provided to employees and officeholders.

Setting up a PSA avoids passing on an unexpected, and potentially demotivating, tax charge to employees. Where a PSA has been agreed with HMRC, this will obviate the need for any reporting on the individual’s P11D.

The items that can be included in the PSA must meet one of three criteria: minor, irregular or impracticable to apply PAYE or apportion between the employees receiving the benefit.

Although reporting will eventually go online, applications for a PSA are currently made in writing to HMRC. The Revenue will then issue a P626 contract, which states that the employer will pay the tax and National Insurance liability on agreed benefits.

BUT NOT TRAVEL COSTS FOR NON-EXECUTIVE DIRECTORS IN PUBLIC SECTOR

Until recently, HMRC allowed taxable travel expenses to be included in public sector PSAs in respect of normal commuting costs for Non-Executive Directors (NED). The Department of Business (BEIS) wrote to the bodies it oversees on 30 May 2019 instructing them that any payments for commuting made to non-executives and other office holders, will now have to be paid through payroll, with tax and National Insurance deducted at source.

Note also that fees for NED roles in the public and private sectors are always required to be subject to tax and NI through the payroll, as this is income for the holding of an office so it cannot be invoiced and paid gross to the NED.

MORE COMPLICATED PENSION RULES

Last month we highlighted the restricted annual pension allowance for those with high income, such as doctors. Note that the deadline for requesting for the additional tax to be paid out of the fund for 2017/18 is 31 July 2019.

There is a further complication for those individuals who have started drawing income from certain money purchase pension schemes. A new £4,000 limit introduced from 6 April 2017 restricts the amount that they can save in their pension and receive tax relief. Our concern is that many taxpayers may unwittingly trigger a tax charge due to this rule change.

NEW VAT RULES FOR THE CONSTRUCTION SECTOR

Under new rules due to come in on 1 October 2019 builders, sub-contractors and other trades associated with the construction industry will have start using a new method of accounting for VAT.

Under the new rules, supplies of standard or reduced-rated building services between VAT-registered businesses in the supply chain will not be invoiced in the normal way. Under the reverse charge, a main contractor would account for the VAT on the services of any sub-contractor and the supplier does not invoice for VAT. The customer (main contractor) would then account for VAT on the net value of the supplier’s invoice and at the same time deduct that VAT from the payment to the sub-contractor.

This is intended to ensure that VAT is correctly accounted for on supplies by sub-contractors.

The new reverse charge will apply to a wide range of services in the building trade, primarily those activities covered by the construction industry (CIS) payment rules. Note that normal VAT invoices will continue to be issued to domestic customers.

Please contact us if you are likely to be affected by these changes and we can work with you to ensure you are ready for the new system.

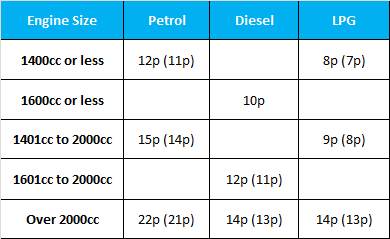

ADVISORY FUEL RATES FOR COMPANY CARS

These are the suggested reimbursement rates for employees' private mileage using their company car from 1 June 2019. Where there has been a change the previous rate is shown in brackets.

Note that for hybrid cars, use the equivalent petrol or diesel scale charge. However, it may be more beneficial to compute the actual cost. You can continue to use the previous rates for up to 1 month from the date the new rates apply.

DIARY OF MAIN TAX EVENTS

JULY/AUGUST 2019

Date

What's Due

01/07/2019

Corporation tax for year to 30/09/2018 (unless pay quarterly)

05/07/2019

Deadline for agents and tenants to submit returns of rent paid to non-resident landlords and tax deducted for 2018/19

06/07/2019

Deadline for forms P11D and P11D(b) for 2018/19 tax year

19/07/2019

PAYE & NIC deductions, and CIS return and tax, for month to 05/07/2019 (due 22/07 if you pay electronically)

31/07/2019

50% payment on account of 2019/20 tax liability due

01/08/2019

Corporation tax for year to 31/10/2018 (unless pay quarterly)

19/08/2019

PAYE & NIC deductions, and CIS return and tax, for month to 05/08/2019 (due 22/08 if you pay electronically)

Location |

Registered as Auditors and regulated for a range of investment business activities in the United Kingdom by the Association of Chartered Certified Accountants Copyright@2018 Mayes Business Partnership Ltd

1974-2024

|

|